Luxury Credit Card Update

This article contains no affiliate links.

As you may know by now, I love my credit cards. Being in the military, and utilizing the benefits of the SCRA, we can get some amazing benefits without having to pay exorbitant fees, especially from the upper echelon cards, or the luxury cards. Depending on your opinion of what constitutes a luxury card – my definition is any card with an annual fee over $200 – you can really live it up! For now, I’ll consider a couple cards as luxury cards – Amex Platinum, Citi Prestige, Chase (JP Morgan) Ritz Carlton, Chase United Club, Visa Black Card, and Citi AA Executive. Of course the Amex Centurion and JP Morgan Palladium are luxury cards, but not many of us, outside of huge spenders, are going to qualify for those. Of the above, I’ve gotten all but the Black Card and the United Club.

First off, the welcome kits with these cards are a little over the top:

Amex Platinum:

Citi Prestige:

Citi AA Executive:

Ritz Carlton:

Each of these welcome kits weighs at least a pound, and has far too much packaging for just having a credit card in it. I think the companies are genuinely trying to drum up excitement about having their card. I have to admit though, that it works – I do get excited when these packages arrive in the mail!

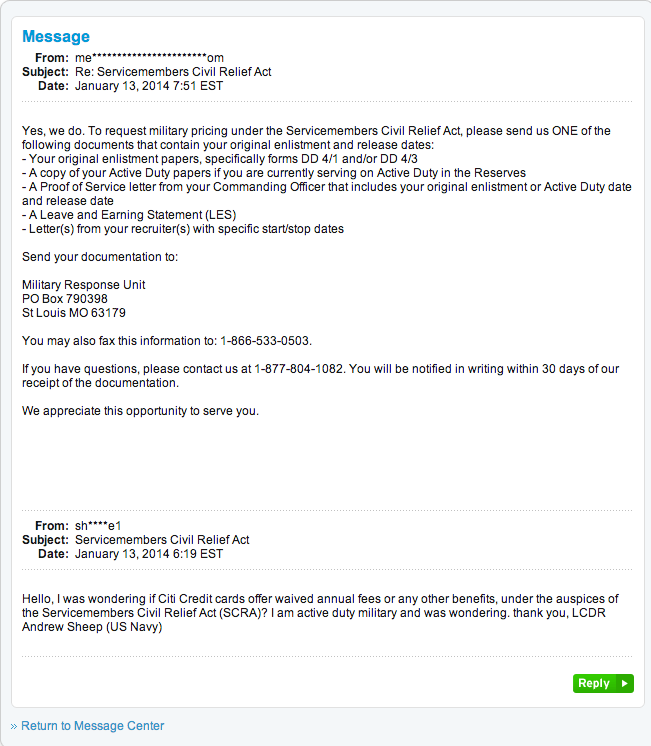

If you’ve read my articles before, you know that you can get your annual fees waived by being in the military. And in the cases of these cards, that’s huge! Just as a reminder – how to get your annual fees waived on American Express cards, how to get your annual fees waived on Citi cards, how to get your fees waived on Chase cards.

Amex Mercedes Benz Platinum annual fee: $475

Citi Prestige Annual Fee: $450

Citi Executive Annual Fee: $450 (I have two of these, so $900)

Chase (JP Morgan) Ritz Carlton Visa Annual Fee: $395

Total money I’ve saved because I’m in the military: $2,225 just for these four cards!! Now, on to the main benefits of having these cards.

For the Amex Plat, the two main perks are the annual $200 airline fee waiver and the airline lounge access, both Centurion lounge and Priority Pass select. The fees are ostensibly only supposed to cover things like baggage fees, in-flight purchases, etc., but can be used for airline gift cards (check out this flyertalk post). Unfortunately, you can only use it for one airline per year, and need to designate it beforehand. And, if you have the opportunity to visit a Centurion lounge a couple times per year, you know how truly nice they are! They’re currently available in DFW, LGA, LAS, and SFO, and will seen be available in both MIA and SEA. Also, because of their frequent Amex Sync offers, having an extra card to sync is huge. Finally, automatic SPG Gold status is pretty awesome too!

For the Citi Prestige, I think it’s combination of benefits is the best out of all of these. First off, you get $250 of airline credit per year, and it can be any airline and go towards any airline fee, including tickets! This is way more useful than unspecified airline fees! You also get the Priority Pass select. Another awesome benefit, one that is not talked about a lot, is their golfing benefit. You get 3 free rounds per calendar year, at a huge selection of courses, available through the Prestige site. During my recent trip to Las Vegas, I played at Bali Hai (typical greens fee $250), Rhodes Ranch ($65), and finally the gorgeous TPC Las Vegas ($199). That’s over $500 for free!

The Citi AA Executive doesn’t offer a whole lot of extra bonuses for it’s annual fee, other than US Airways and American Admiral’s Club lounge access. The main reason to sign up early last year was for 100k AA miles (that offer is no longer available). There is a current offer for 50k AA miles after $5000 spend, and $450 annual fee. Not worth it to me.

Finally, I recently signed up for the Chase (or JP Morgan) Ritz Carlton Visa Signature card, which gives 140k Ritz Carlton or Marriott points after $2k in spend, and with a $395 annual fee. The most obvious benefit, other than the points, is the Marriott Gold status for the first year (and each year after w/ $10k spend), but I think the biggest benefit is the $300 of airline fee credit per year. This, like the Amex Plat, is only supposed to go towards actual fees, but also like above, can go towards airline gift cards (check out this post about it by Doctor of Credit).

As you can see, I’ve not only saved a lot of money on not paying annual fees, but also gotten a ton of money’s-worth benefit out of having these four awesome cards. If you’re in the military and have a good credit score, I’d highly recommend checking these out.

{kind=link}

{kind=link}

Sir, is there any way a reservist or guard can get this who hasn’t been activated for 30 days or more? perhaps going to professional military school for a week or so?

I am so glad you posted this. I have been researching all day for a new card. I think at this point the best for us is the AMEX Platinum because we won’t be doing much travel in 2015 due to pregnancy/new baby. The 40k MR won’t expire unlike airline mileage. Also, I can get gift cards for the $200 fee credit and save them for next year.

The Prestige looks enticing but again, I don’t think we’d utilize it.

Any suggestions?

@Mary – I’d consider the Mercedes Benz version of the Plat if you’re going to get one, as it offers 50k MR vs 40k for the regular one. I’m going to call the Visa Black phone line sometime this week or the next and see if that card qualifies for SCRA benefits.

@Ryan1 – The only way I can see about doing it is getting activated, ie actually having active duty orders. If military school will get you that, and the credit card company can be convinced that you’re active, then you should be good to go. Most of them base their definition of active or not on DEERS data.

Outside of Amex and Capitalone, the results are mixed on comping fees for regular active duty troops with these credit cards.

Caveat emptor.

What do you base the results are mixed on comping fees comment on Jerry? Have you tried the process from the links above with Cit and Chase? Anybody other AD not get fees waived with Citi or Chase?

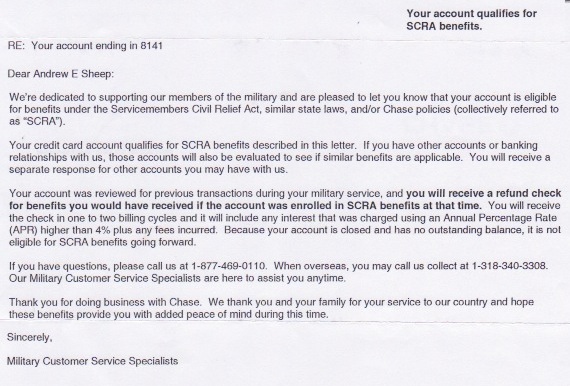

Just called Chase and they follow the SCRA to the letter, and will not waive unless you had an account with them prior to service.

I messaged Chase earlier this week for waived fees on my CSP account. My husband is AD and they waived the fees on my CSP where he is an authorized user. They required his orders and a marriage certificate.

I’d suggest sending a secure message instead.

I agree that Amex and CapOne are easy as can be. Chase can take some cajoling, although I’ve found they’ll waive fees if you really press them. I have two readers, both reservists, that Chase is waiving their fees. Citi is really a stickler, and requires faxing in of orders, DD214, etc. So in a sense, it is caveat emptor. In the above cases, I think that for all four cards, even without the fees waived, they would’ve made sense to get at least for a year, based on their benefits, which to me outweighed the fees.

How did you get CIti to waive fees since you got card after your first day of active duty? I am having a good deal of trouble getting them to waive fee for the prestige card.

Dear Sirs,

sadly, I represent a negative data point. I’ve tried your methods to get the annual fees waived for both Chase (CSP) and Amex (currently PR Gold, was considering Plat), but they offered “other” benefits not including waived Annual Fee. At least these tips have apparently worked sometimes for some people.

@Joseph

Did you get your card/s before or after becoming Active Duty?

I successfully got my fees waived for the AMEX Platinum 2 weeks ago, they also waived fees for my wife when we signed her up. 2 Amex Plats + no ann fee = no guest charge at lounges and a smile (or 2)

Any luck on getting the Visa Black annual fee waived?

@Connor – I was just thinking about this last night. I’d called the number 3 separate times, but none of those 3 reps could give me any definitive info on SCRA and waiving the annual fee. They all gave me a version of, “just apply and call back”, but that’s a rather large annual fee to pay if I’m not guaranteed to get it waived. I’m not going to lie, I”m a little reticent to apply for it just for an experiment to see if I can get the fee waived.

Plus one for AD being denied for CSP annual fee waiver. Their cited reason was I got the card after joining. I tried via secure messaging and the military phone line that they provided via secure messaging.

I recently got the AMX Platinum with the 100k MR bonus! So glad I waited for the bonus to come around again!

Sir, I recently got the Citi Thank You Premier thinking they would waive the $95 fee. I had seen that you had success getting them to waive in previous posts. However, the military affairs folks have been denying me this and keep stating that they will only do it if I had the card before I entered the military. Any advice on how to talk to at Citi about this and get them to waive the fee?

I believe this post ought to be updated…I think things have changed since this was originally published and credit card companies are clearly “wisening up” and strictly enforcing their current policy as below. The tone of this post may be misleading if it is read as a “definitely will work” strategy.

Buyer beware…definitely recommend calling to verify before you apply. Just went through the online application and called Citi’s military line to confirm the fees would be waived and I was told by two separate members (I called twice to see what they would say) that it ONLY applies to Active Duty who had a balance on their account the day they came on active duty. In other words – unless you had the card PRIOR to your Active duty date, you are SOL.

Also confirmed: Citi will NOT lower APR or waive annual fee for cards opened after starting Active Duty.

I have had success with fees with Chase (Military Line), Capital One, Barclaycard, and AMEX Platinum all within the last two months. All fees and Apr lowered to 4% or lower. I dont have a Citi card but seems like they are harder to work with than others. I really would like the Citi Prestige for that golfing perk and airline credit!

So,

my question is, these benefits sound awesome and i’m all for the perks BUT for those of us who will likely be exiting the military in a few years and will thus be immediately cancelling all of these lines of credit IOT avoid the annual fees… how negatively do you think that will hurt our credit scores?